Imagine a young boy, age 10 or so, decides to save for college. He saves for 8 years, and since he is under age, his parents are custodians on the account. Upon high school graduation applies for college. At that point, his parents regretfully inform him that he has no money to go to college. He asks where his college fund went. They reply that a few years ago, when money was short, they dipped into his college fund to pay the rent. A few years later, they dipped into it again to fund a vacation. Whatever the reason, the money is gone, and the son is out of luck.

What is owed to the son? Who owes it? Obviously, at the least, the son is owed what he put in. And obviously, the parents owe that money to the son. The parents SHOULD have used their own money for those other expenses, but they didn't.

This is the same as our current situation. We, like the son, have put in money for years. The government, like the parents, spent the money (which SHOULD have remained in trust) on other things--previous years' recipients, as well as other miscellaneous expenses through the years. Congress used funds from Social Security to fund pet projects and make it appear that the national debt was lower than it actually was.

That's right--technically the lack of a Social Security trust fund is an off the books addition to the national debt.

Thursday, October 6, 2011

Monday, May 9, 2011

The Federal Debt--a dose of perspective

The federal budget, budget deficit, and national debt are big news items. As we discuss them, big numbers like billions and trillions get thrown around, and in the process we get numb to the idea of what we're talking about. It seems a bit of perspective is in order.

First, some definitions so that we all are on the same sheet of music. First of all the federal budget, like you would probably guess, is the total expected income and expenditures by the federal government for one year--pretty much like a family budget. The deficit is the amount that expenditures exceed the income in that year. Think of it as what we as a country charge on our credit card that year only. The debt is the sum total of all the deficits up to now, including the interest. Think of that as your total credit card balance.

OK, so our current national debt as I write this is just over 14 trillion dollars. How much is that?

Let's say you have a millionaire. Now let's get a LOT of millionaires. In fact, let's fill a major sports stadium (one that holds around 100,000 people) with millionaires. Once that stadium is filled with 100,000 millionaires, you are now up to 100 billion dollars. Ten of those stadiums would get you to one trillion dollars. It would take 140 stadiums filled with 100, 000 millionaires to get to 14 trillion dollars. So how many millionaires would that be? That's 14 million millionaires!

Let's say you have a millionaire. Now let's get a LOT of millionaires. In fact, let's fill a major sports stadium (one that holds around 100,000 people) with millionaires. Once that stadium is filled with 100,000 millionaires, you are now up to 100 billion dollars. Ten of those stadiums would get you to one trillion dollars. It would take 140 stadiums filled with 100, 000 millionaires to get to 14 trillion dollars. So how many millionaires would that be? That's 14 million millionaires!

So... if we were to fix this by "taxing the rich", we would have to find 14 million millionaires and take everything they own to pay off the debt. I'm going to go out on a limb here and guess that's not going to happen, so I think we can see that this isn't the answer.

To pay off the debt, we have to run a budget surplus, meaning that we bring in more than we spend. As I mentioned in a previous blog post, Congress has been notoriously bad at this, but it's something we simply have to force them to do immediately. Why, you ask? Good question...

If we spent no more than we brought in, we'd NEVER pay off the debt--we'd just be marking time exactly where we are. So if we had a surplus on $1 billion dollars per year, how long would it take to pay off the debt? $14 Trillion divided by $1 billion is 14,000 years! If we managed to get a surplus of $100 billion a year, it would still take 140 years. (For perspective, the current House Republican plan only calls for $61 billion in spending cuts, and it's being hailed as too aggresive.)

If we spent no more than we brought in, we'd NEVER pay off the debt--we'd just be marking time exactly where we are. So if we had a surplus on $1 billion dollars per year, how long would it take to pay off the debt? $14 Trillion divided by $1 billion is 14,000 years! If we managed to get a surplus of $100 billion a year, it would still take 140 years. (For perspective, the current House Republican plan only calls for $61 billion in spending cuts, and it's being hailed as too aggresive.)

Now here's the bad news... we aren't anywhere near breaking even, even with those "aggressive" cuts. In 2009, the federal budget deficit was $1.4 TRILLION dollars. That means that just to break even (or "balance the budget"), we'd have to make $1.4 trillion in cuts just to start out. Then on top of that, we'd need to come up with still more money to pay down what we've already spent.

If we set a reasonable goal, say 50 years, to pay off the debt, we would need to cut current spending levels by $1.7 trillion dollars. Each and every year for the next 50, we would have to make sure we spent $480 billion less than we take in in order to get there.

One last bit of perspective. The current population as of the latest census was 308 million people. If you divide up the $14.362 trillion deficit evenly among each person in the country, the amount comes to about $46,000 for each and every person. Married couples--you owe $92,0000. Family of five--$234,000. That's YOUR SHARE of this debt--and it belongs to each and every one of us, whether we like it or not.

One last bit of perspective. The current population as of the latest census was 308 million people. If you divide up the $14.362 trillion deficit evenly among each person in the country, the amount comes to about $46,000 for each and every person. Married couples--you owe $92,0000. Family of five--$234,000. That's YOUR SHARE of this debt--and it belongs to each and every one of us, whether we like it or not.

So... when you hear about "draconian" cuts to the federal budget, remember this--until our cuts exceed $1.4 trillion dollars, the ship is still sinking. And if we ever hope to save this ship, we need to do even better than that.

First, some definitions so that we all are on the same sheet of music. First of all the federal budget, like you would probably guess, is the total expected income and expenditures by the federal government for one year--pretty much like a family budget. The deficit is the amount that expenditures exceed the income in that year. Think of it as what we as a country charge on our credit card that year only. The debt is the sum total of all the deficits up to now, including the interest. Think of that as your total credit card balance.

OK, so our current national debt as I write this is just over 14 trillion dollars. How much is that?

So... if we were to fix this by "taxing the rich", we would have to find 14 million millionaires and take everything they own to pay off the debt. I'm going to go out on a limb here and guess that's not going to happen, so I think we can see that this isn't the answer.

To pay off the debt, we have to run a budget surplus, meaning that we bring in more than we spend. As I mentioned in a previous blog post, Congress has been notoriously bad at this, but it's something we simply have to force them to do immediately. Why, you ask? Good question...

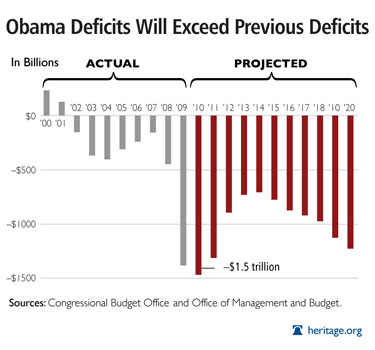

|

| Source: Heritage Foundation |

Now here's the bad news... we aren't anywhere near breaking even, even with those "aggressive" cuts. In 2009, the federal budget deficit was $1.4 TRILLION dollars. That means that just to break even (or "balance the budget"), we'd have to make $1.4 trillion in cuts just to start out. Then on top of that, we'd need to come up with still more money to pay down what we've already spent.

If we set a reasonable goal, say 50 years, to pay off the debt, we would need to cut current spending levels by $1.7 trillion dollars. Each and every year for the next 50, we would have to make sure we spent $480 billion less than we take in in order to get there.

So... when you hear about "draconian" cuts to the federal budget, remember this--until our cuts exceed $1.4 trillion dollars, the ship is still sinking. And if we ever hope to save this ship, we need to do even better than that.

Thursday, March 3, 2011

Tax increases won't fix debt problem

A recent NY Times poll states, among other things, "Asked how they would choose to reduce their state’s deficits, those polled preferred tax increases over benefit cuts for state workers by nearly two to one."

The argument of tax increases vs. spending cuts is a popular one in politics today, but it is the epitome of a red herring. To listen to the talking heads, either one is a valid option to solve the budget crises that plague both state and federal budgets. However, in this case, all things are not equal.

The debt crisis which has arisen did not occur due to a lack of funds. Federal and state revenues have steadily risen. The problem results from one very simple cause--no matter how much money governments bring in, they are spending more than that.

This is a very familiar scenario for most people who have gotten deeply into debt. It might start shortly after first becoming employed. You spend more than you make in anticipation of "making more next year." And you DO make more next year--but you also SPEND even more. But that's okay, because you'll make more next year. And so on. And so on. Despite a continually increasing salary, you find yourself deeper and deeper in debt. More income did NOT solve the debt crisis.

This problem can only be stopped (and later solved) in one way--by reducing spending below income. Once that has been achieved, then future income increases WILL actually lower your debt level IF you continue to live within your means.

For the last several decades, we as a nation have become addicted to debt, both in public and in private. No matter the tax revenue, spending has outpaced it. Regardless of how much money you hand to Congress, they have no problem spending it, and more. If we increased the tax rate to 100% and handed the entire GDP to Congress, under the current mindset they would spend 105% of it.

It is ESSENTIAL that we get spending under control. We can no longer afford as a nation to continue in this manner. Often when this comes up, someone will ask, "why is this a big deal NOW? The other party did it, too..." Unfortunately, that's correct--both parties have been guilty of this. As to why it has become more important now, well, two things are bringing this issue to a head.

First of all, returning to the example of a family running up credit card debt, our salary (the nation economy) is no longer steadily growing. The economy has become stagnant (or shrinking at times) with nothing on the horizon to improve it. We can't cover the bills any longer.

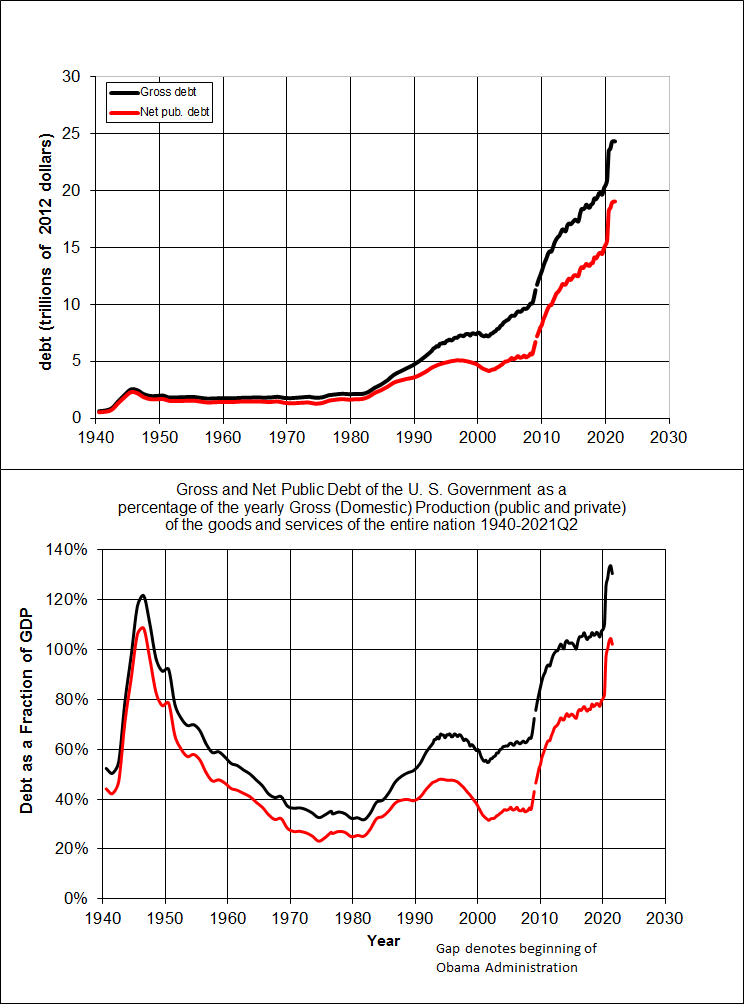

Second, as anyone who has ever sat through a presentation on investments is aware, compound interest eventually wins the day. When our debt was low and we paid large payments on it, the situation was not a crisis. But as the debt piled up (and so did the interest), the compounding interest began climbing the exponential curve toward oblivion. If you look at debt as a percentage of gross domestic product , you see how steeply the curve has risen over the last 3-4 years. Unless GDP begins growing again (immediately, rapidly and strongly) there is no way that we can get our debt situation under control.

Rather than try to solve the problem, Congress has tried to do even more of the same. For many years, our primary deficit (difference between revenue and spending, not including interest on the debt) wasn't so great. However, recently the primary deficit has increased. Add to that the fact that the total deficit (deficit including interest on the debt) has increased, and the situation becomes grave.

It is important that we as a nation become educated about our debt or it could soon devolve into a crisis unseen in this country's history (including the Great Depression). We must NOT hand more money to lawmakers, no matter how well intentioned--it would be like throwing gasoline onto a fire.

The argument of tax increases vs. spending cuts is a popular one in politics today, but it is the epitome of a red herring. To listen to the talking heads, either one is a valid option to solve the budget crises that plague both state and federal budgets. However, in this case, all things are not equal.

The debt crisis which has arisen did not occur due to a lack of funds. Federal and state revenues have steadily risen. The problem results from one very simple cause--no matter how much money governments bring in, they are spending more than that.

This is a very familiar scenario for most people who have gotten deeply into debt. It might start shortly after first becoming employed. You spend more than you make in anticipation of "making more next year." And you DO make more next year--but you also SPEND even more. But that's okay, because you'll make more next year. And so on. And so on. Despite a continually increasing salary, you find yourself deeper and deeper in debt. More income did NOT solve the debt crisis.

This problem can only be stopped (and later solved) in one way--by reducing spending below income. Once that has been achieved, then future income increases WILL actually lower your debt level IF you continue to live within your means.

For the last several decades, we as a nation have become addicted to debt, both in public and in private. No matter the tax revenue, spending has outpaced it. Regardless of how much money you hand to Congress, they have no problem spending it, and more. If we increased the tax rate to 100% and handed the entire GDP to Congress, under the current mindset they would spend 105% of it.

It is ESSENTIAL that we get spending under control. We can no longer afford as a nation to continue in this manner. Often when this comes up, someone will ask, "why is this a big deal NOW? The other party did it, too..." Unfortunately, that's correct--both parties have been guilty of this. As to why it has become more important now, well, two things are bringing this issue to a head.

First of all, returning to the example of a family running up credit card debt, our salary (the nation economy) is no longer steadily growing. The economy has become stagnant (or shrinking at times) with nothing on the horizon to improve it. We can't cover the bills any longer.

Second, as anyone who has ever sat through a presentation on investments is aware, compound interest eventually wins the day. When our debt was low and we paid large payments on it, the situation was not a crisis. But as the debt piled up (and so did the interest), the compounding interest began climbing the exponential curve toward oblivion. If you look at debt as a percentage of gross domestic product , you see how steeply the curve has risen over the last 3-4 years. Unless GDP begins growing again (immediately, rapidly and strongly) there is no way that we can get our debt situation under control.

{kind=link}

(Image from http://en.wikipedia.org/wiki/United_States_public_debt )

Rather than try to solve the problem, Congress has tried to do even more of the same. For many years, our primary deficit (difference between revenue and spending, not including interest on the debt) wasn't so great. However, recently the primary deficit has increased. Add to that the fact that the total deficit (deficit including interest on the debt) has increased, and the situation becomes grave.

It is important that we as a nation become educated about our debt or it could soon devolve into a crisis unseen in this country's history (including the Great Depression). We must NOT hand more money to lawmakers, no matter how well intentioned--it would be like throwing gasoline onto a fire.

Thursday, January 27, 2011

Great Milton Friedman quote

A friend of mine posted this Milton Friedman quote today on Facebook:

"If you pay people not to work and tax them when they do, don't be surprised if you get unemployment."How does this not appear obvious to Congress, and the public at large?

Subscribe to:

Posts (Atom)